Fed action -- if it happens -- is no longer viewed as the elixir for the stock market it once was.

Wall Street tumbled over 2 percent on Friday as investors fretted more about the economic outlook rather than looking ahead to another round of Fed bond buying.

Next week, the question of whether the Fed will step up to the plate with another round of quantitative easing will take center stage with a highly anticipated speech from President Barack Obama. That could make for another volatile week.

This time last year, anticipation of a second round of quantitative easing, or QE2, sparked an almost uninterrupted rally that lifted the S&P 500 around 30 percent from August to May.

What a difference a year makes. Confidence in policy makers is sapping away as the economy languishes, the United States grapples with the loss of its top-notch credit rating, and the European Union seems to be coming undone at the seams.

Wall Street sees an 80 percent chance the Federal Reserve will intervene in the bond market to lower long-term interest rates, according to a Reuters poll on Friday.

But Friday's action in the stock market signaled that equity investors do not see that prospect as silver bullet for their woes. The broad-based S&P 500 .SPX index fell 2.5 percent on the day.

"This downdraft is based on sentiment and that has to be turned around," said Brian Battle, vice president of trading at Performance Trust Capital Partners in Chicago. "I think we're in for a longer trend of either malaise or just a down channel."

That means traders and investors who were hoping for a return to normalcy after extreme volatility in August may have to wait a little longer.

Obama is due to address a joint session of Congress on Thursday to lay out plans to create jobs, boost economic growth and lower the deficit.

He faces an uphill struggle when it come to reassuring investors, who fault the lack of consensus in Washington. Heading into an election year, the disharmony is not likely to get better any time soon.

Nonfarm payrolls were unchanged last month, the Labor Department said on Friday, and figures for previous months were also revised down to show employers created a combined 58,000 fewer jobs than had been thought in June and July.

The U.S. Treasury market rallied after the data as Goldman Sachs and other U.S. primary dealers -- big Wall Street firms that do business directly with the Fed -- said they expect the U.S. central bank to start buying longer-dated bonds after its September 20-21 meeting.

Seasoned traders say that August's extreme volatility was one of the most trying periods in living memory, outstripping the 2008-2009 meltdown and the 1987 stock market crash on Black Monday.

"I've been doing this for 20 years and it's never been more exhausting," said the chief executive of a New York-based proprietary trading firm, who said many of his traders closed out their positions in August, reducing the firm's inventories to just 15 to 20 percent of what they could be.

At least some of that volatility looks set to spill over into September until there is more clarity over the economy and what the Fed is likely to do at its September 20-21 meeting.

But some fund managers who take a more long-term view are using pullbacks to cut back positions that have done less well while increasing positions in their preferred stocks.

Many fund managers are still convinced the U.S. economy will avoid a recession and stocks will rally into the end of the year.

One of them, Mark Luschini, chief investment strategist at Janney Montgomery Scott in Philadelphia, does not expect the Fed to act this month. He is not expecting a recession, but admits he has become more defensive.

"We used some of the volatility to swap out lower yields for higher yields, believing that a combination of income with capital growth potential will help us weather days like today," he said. "Equity values should still hold their own if not appreciate given the still-good corporate profit picture."

Source

Sunday, September 4, 2011

Thursday, July 14, 2011

Retirees May Want to Consider HECM for Purchase

Is it logical—or even possible—for a 69-year-old to get a mortgage? a prospective home-buyer wonders in a recent Wall Street Journal column. The short answer is yes, it’s possible, although there are other options to be considered, including a reverse mortgage—or specifically, a HECM for purchase, WSJ says.

The home-buyer in question is looking to sell his current residence in order to buy a retirement home. He says he could pay all cash for the house he’s interested in, but is thinking about taking advantage of low interest rates rather than tying up all of his money in real estate.

As long as you meet a lender’s requirements as far as income, credit, and other related factors, says WSJ, you’re eligible for a mortgage, no matter what your age, under the federal government’s Equal Opportunity Credit Act. If the borrower were to pass away before the mortgage is paid off, the unpaid balance would become a lien tied to the house, and heirs would be obligated to either make the remaining payments on the mortgage, sell the house to pay off the mortgage, or refinance the loan.

However, the article continues, another option that should be considered at the prospective buyer’s age is a reverse mortgage. Thanks to the Housing and Economic Recovery Act of 2008, says WSJ, it may even be possible for the prospective buyer to purchase the new home and get a reverse mortgage in a single transaction as long as all requirements are met. Getting a reverse mortgage allows homeowners to convert their property’s equity into cash which can be accessed through a fixed monthly amount, a line of credit, or both, the article continues.

There are some other things to be considered when contemplating a reverse mortgage, WSJ mentions. These including required reverse mortgage loan counseling, owning the home outright or have a small remaining balance on the mortgage, and remaining in that home as a primary residence.

It may be years before you will see much appreciation on your new home, says WSJ, so it’s recommended to free up at least some cash rather than sinking it all in real estate. - source

The home-buyer in question is looking to sell his current residence in order to buy a retirement home. He says he could pay all cash for the house he’s interested in, but is thinking about taking advantage of low interest rates rather than tying up all of his money in real estate.

As long as you meet a lender’s requirements as far as income, credit, and other related factors, says WSJ, you’re eligible for a mortgage, no matter what your age, under the federal government’s Equal Opportunity Credit Act. If the borrower were to pass away before the mortgage is paid off, the unpaid balance would become a lien tied to the house, and heirs would be obligated to either make the remaining payments on the mortgage, sell the house to pay off the mortgage, or refinance the loan.

However, the article continues, another option that should be considered at the prospective buyer’s age is a reverse mortgage. Thanks to the Housing and Economic Recovery Act of 2008, says WSJ, it may even be possible for the prospective buyer to purchase the new home and get a reverse mortgage in a single transaction as long as all requirements are met. Getting a reverse mortgage allows homeowners to convert their property’s equity into cash which can be accessed through a fixed monthly amount, a line of credit, or both, the article continues.

There are some other things to be considered when contemplating a reverse mortgage, WSJ mentions. These including required reverse mortgage loan counseling, owning the home outright or have a small remaining balance on the mortgage, and remaining in that home as a primary residence.

It may be years before you will see much appreciation on your new home, says WSJ, so it’s recommended to free up at least some cash rather than sinking it all in real estate. - source

California real estate analyst G.U. Krueger adds his commentary on the housing market

It’s no secret that fast growing emerging nations like Brazil, China, and India represent major investment opportunities, especially for real estate.

One wonders why this nation’s homebuilders haven’t quite got this. May be they should look into this, given the languishing housing demand in the homeland.

In this context, it is interesting that CalPERS just released a press release saying that it and Hines, an international investment firm, earned $160 million from the closing of a Brazilian real estate fund, i.e. the sale of office, residential, and logistics projects in Sao Palo, Rio De Janeiro, Curitiba and other cities. The rate of return over the six-year investment period was a stunning 60%, triple the initial 20% target rate, not bad.

The success was achieved “through a strategic asset investment thesis leveraging off internal growth in Brazil’s emerging economy”, according to a Hines press release. Sounds smart, and CalPERS, who is in the process of acquitting itself from its experience with U.S. housing in its investment, is looking for more “leveraging”. According to its press release on the matter, the Brazilian connection is an ”affirmation of our new strategy to deploy up to 15% of our real estate capital to growth markets like Brazil and China.”

Clearly, growing middle classes in emerging countries provide “favorable demand for the development of shopping centers, warehouses, offices and residential units.”

One wonders why U.S. builders and developers haven’t made a big plunge into the foreign sector, yet. Is it too risky or is it just too much work? On the face of things, they could add a lot expertise to these markets.

Exporting “Orange County” real estate styles and development designs could be an untapped competitive advantage for U.S. builders if they could go from local to global. Some competitive edges U.S. builders might have:

Architectural and land development design. Some California architectural firms — like the Dahlin Group — are working with Chinese builders. •

Financial and project proforma wizardry with access to global financial centers.

Great sensitivity of what growing middle-class customers want

Our master-planned communities. They’re a “brand” already in those countries, because their citizens have bought new homes in the U.S.

Corporate infrastructure that can bring greater efficiencies to the residential construction sector abroad.

Yes, there are risks, different rules and regulations, issues with the repatriation of profits, different business practices and culture, but it might be worth a try. Leverage emerging economies, young real estate person. source

One wonders why this nation’s homebuilders haven’t quite got this. May be they should look into this, given the languishing housing demand in the homeland.

In this context, it is interesting that CalPERS just released a press release saying that it and Hines, an international investment firm, earned $160 million from the closing of a Brazilian real estate fund, i.e. the sale of office, residential, and logistics projects in Sao Palo, Rio De Janeiro, Curitiba and other cities. The rate of return over the six-year investment period was a stunning 60%, triple the initial 20% target rate, not bad.

The success was achieved “through a strategic asset investment thesis leveraging off internal growth in Brazil’s emerging economy”, according to a Hines press release. Sounds smart, and CalPERS, who is in the process of acquitting itself from its experience with U.S. housing in its investment, is looking for more “leveraging”. According to its press release on the matter, the Brazilian connection is an ”affirmation of our new strategy to deploy up to 15% of our real estate capital to growth markets like Brazil and China.”

Clearly, growing middle classes in emerging countries provide “favorable demand for the development of shopping centers, warehouses, offices and residential units.”

One wonders why U.S. builders and developers haven’t made a big plunge into the foreign sector, yet. Is it too risky or is it just too much work? On the face of things, they could add a lot expertise to these markets.

Exporting “Orange County” real estate styles and development designs could be an untapped competitive advantage for U.S. builders if they could go from local to global. Some competitive edges U.S. builders might have:

Architectural and land development design. Some California architectural firms — like the Dahlin Group — are working with Chinese builders. •

Financial and project proforma wizardry with access to global financial centers.

Great sensitivity of what growing middle-class customers want

Our master-planned communities. They’re a “brand” already in those countries, because their citizens have bought new homes in the U.S.

Corporate infrastructure that can bring greater efficiencies to the residential construction sector abroad.

Yes, there are risks, different rules and regulations, issues with the repatriation of profits, different business practices and culture, but it might be worth a try. Leverage emerging economies, young real estate person. source

Housing Prices, and the Great Stagflation

Back in April, Floyd Norris of the New York Times wrote one of the most insightful articles I have encountered recently. He decided to look at CPI if home prices continued to be included in the index after 1983. This, of course, requires a little bit of explanation.

Prior to 1983, the US Consumer Price Index included housing prices. A change was made at that time, however, to replace housing prices with a concept called “owners’ equivalent rent.” The rationale behind this change was that CPI should not include “investments” and home ownership was both consumption and investment. “Owners’ equivalent rent” was measured not by housing prices, but by rental prices given up by the homeowner in order to occupy the unit. In this way, it was hoped to strip out the “investment” related aspect of housing, while still holding onto the consumption aspect of it.

Unfortunately, this minor change in the way CPI was measured has had dramatic results on the end product. It’s created a situation where the Federal Reserve and other government actors are looking at one set of statistics to measure inflation, when the economic reality can be completely different. This is not to argue that there is a conspiracy to engineer the statistics, as some have suggested. Rather, a minor change in methodology has merely changed the way we perceive things in a detrimental fashion.

Alternative Economics

I’ve become enamored by how the disparity between official economic statistics and economic reality might have caused poor decision making by both the public sector and the private sector. As a result, I’ve launched a website, Alternative Economics, dedicated to exploring this issue in more detail. The centerpiece of my efforts is an Alternative CPI measure based on housing prices. From this, I’ve also re-examined GDP growth and monetary policy. The results have been paradigm-shifting, to say the least.

After viewing the economy under the lens of “Alternative CPI,” the US appears to have had negative real economic growth from 2000 to 2006. With high nominal GDP growth offset by even higher inflation, this period would be most properly termed “The Great Stagflation” or alternatively, “The Great Inflationary Depression.”

In this sense, 2000 – 2006 was the worst period in American economic history since the Great Depression and the ‘70s Stagflationary Era. While I’ve drawn several conclusions using my data, for now, I want to focus on my concept of Alternative CPI to show you why it’s more accurate and why it should change the way you think about the 2000s.

Alternative CPI Methodology

One major reason why housing price data is vital for any realistic inflation measure in the United States is because so much of American consumption is related to housing. Roughly 65% of Americans are homeowners and we have a society that views home ownership as an important goal in life. Mortgage payments often make up anywhere from 25% – 40% of monthly income for many Americans, making it a major cost.

Due to the effect of leverage in the housing market, it is one of the areas of consumer expenditure where prices are most likely to become inflated due to an excess supply of money. Given this, to ignore housing prices in inflationary measures is pure folly. Indeed, what’s the point of even examining CPI inflation if it ignores the most pertinent item in most American’s budgets?

For my conception of Alternative CPI, I’ve replaced the BLS’s concept of owners’ equivalent rent, with the S&P /Case-Shiller Home Price Index. This is slightly different than Floyd Norris’ conception in the NY Times, as he uses statistics compiled from Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB). I decided to use Case-Shiller over this for a few reasons, including greater ease of access. Moreover, I would view it as an acceptable proxy for housing prices across the country.

In spite of the fact that urban housing prices would tend to rise more in a boom than rural prices, the majority of the American populace lives in a major metropolitan area. Urban housing prices would also be a better indicator of dangers in the real economy.

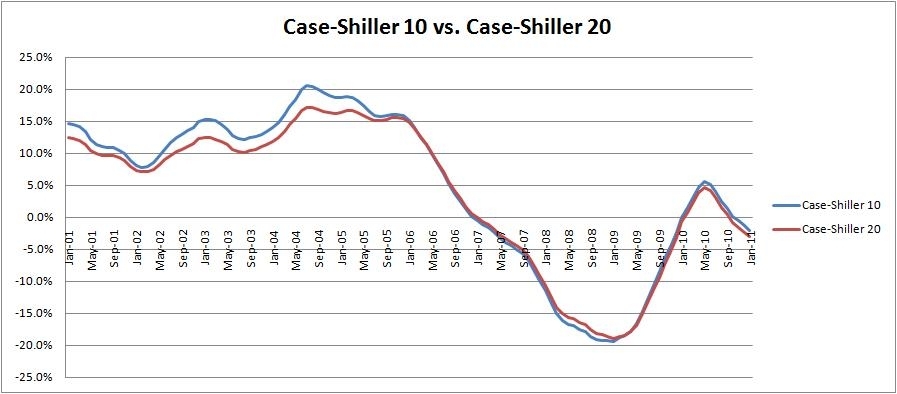

With Case-Shiller, there is both a 10-city index and a 20-city index. The 10-city index has a longer history, going back to 1987, while the 20-city index only reaches back to 2000. The obvious advantage with the 20-city index is that it looks at a broader swath of housing data. However, in practice, the two indexes do not dramatically differ from one another, as the chart below suggests - (click charts to enlarge):

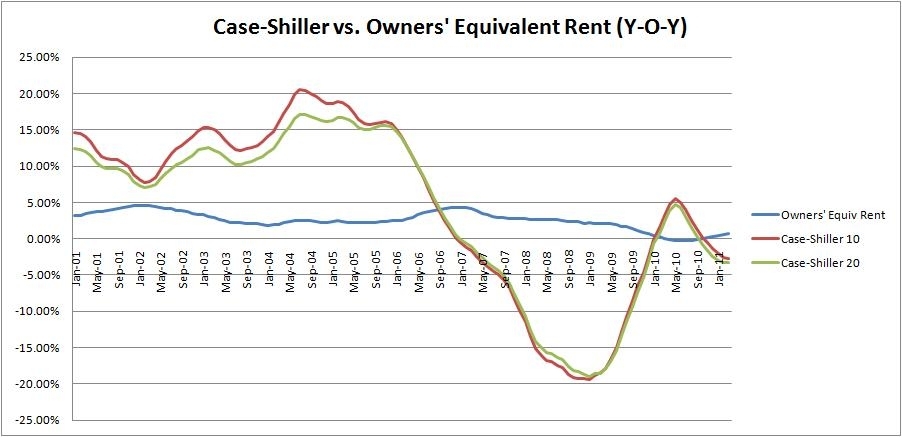

While the Case-Shiller 10-city index does show slightly higher year-over-year increases during the housing boom years, the differences are not that dramatic. In fact, if we take the above chart and add the BLS’s concept of “Owners’ Equivalent Rent” (OER), you will quickly see that the differences between the two Case-Shiller indices are minor compared with the difference between Case-Shiller housing price data and “Owners’ Equivalent Rent.”

Given this, I decided to use Case-Shiller’s 10-city housing price index in order to calculate Alternative CPI. The longer history associated with that index creates a better data set and it’s not a stretch to suggest that the Case-10 can serve as a proxy for a broader metropolitan housing market index.

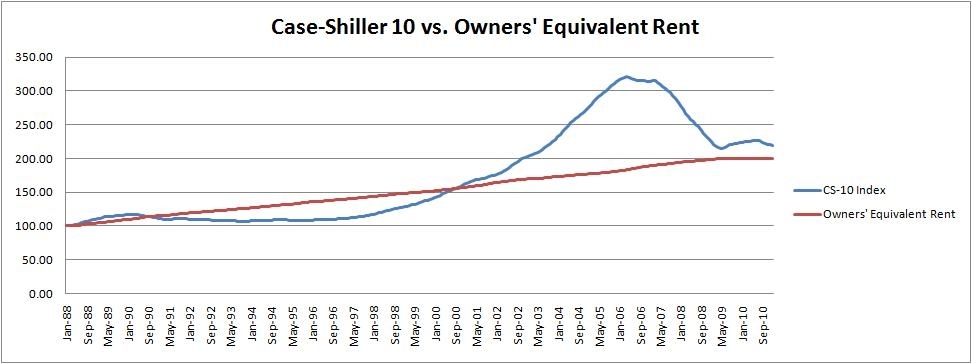

Before jumping to the results of our Alternative CPI, let’s take a look at one final chart examining the Case-Shiller Index versus owners’ equivalent rent. The chart below shows the index values, as opposed to year-over-year increases as in the chart above. The giant hill in the chart represents the housing bubble and you can see that we are just now reaching a point where the Case-Shiller 10-city index and OER are finally closing in on one another again:

Alternative CPI

Due to the failure of OER to capture true price inflation, it’s easy to see why Alternative CPI ends up being such an important concept. OER allowed official inflation figures to be dramatically understated for years and might have hidden major economic problems in the United States during the early 2000s. Moreover, it led to extremely poor policymaking from the Federal Reserve and the US government.

Let’s examine how Alternative CPI differs from official CPI. For my measure, I did not change any inputs in official CPI inflation except OER, which I replaced with the Case-Shiller 10-city housing price index. With this one minor change, CPI looks dramatically different as the chart below shows:

Official CPI and Alternative CPI stay within about a 200 basis point spread of one another from 1988 to 1998. After that, the two figures start to drift apart considerably. By 2004, there is nearly a 700 basis point spread between official CPI and our Alternative CPI measure.

In July ’04, for instance, official CPI records a mild 3.0% year-over-year increase in inflation. While this is lower than the Federal Reserve’s general target, it’s not all that alarming, all the same. 3% is well within US historical averages during healthy economic times.

Alternative CPI, on the other hand, reports a troubling 9.4% year-over-year increase in inflation. If official CPI had reported such a high result, alarm bells would’ve been set off all over the place. 3% is manageable inflation; 9.4% suggests an economy with major problems. In fact, we had already drifted over 6% inflation in 1999 using my Alternative CPI gauge. Alternative CPI cooled off a bit during the tech crash, before eclipsing 6% inflation once again by mid-2002.

Alternative Real GDP

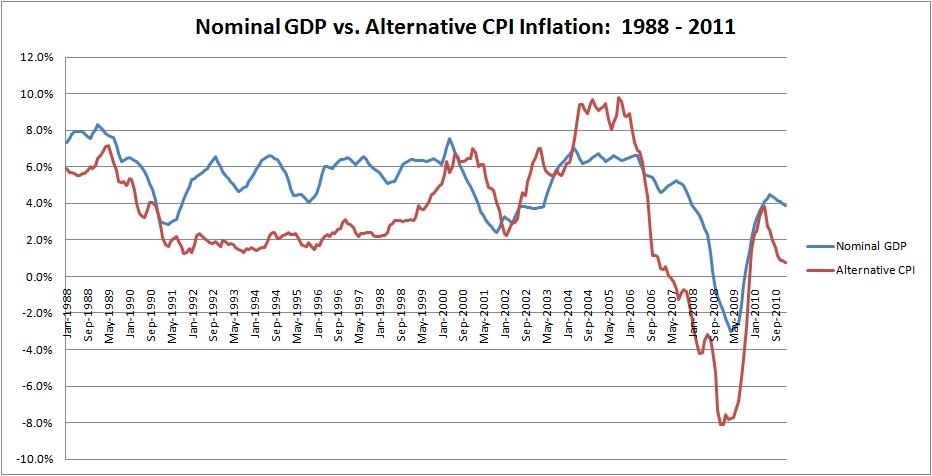

Where this becomes even more profound is when we start looking at the Alternative CPI inflation compared with economic growth and monetary policy. I’m saving the monetary policy discussion for my next article, so for now, we’ll focus on economic growth. This is where our Alternative CPI starts to become “paradigm-shifting.” The chart below examines Alternative CPI versus Nominal GDP:

The best way to read the chart above is to examine both lines to see which one is on top. When the blue line is above the red line, that means that the US was experiencing positive real economic growth. When the blue line is below the red line, that means that price increases were outpacing nominal GDP growth, so that real economic growth was negative. Notice that the 2000 to 2006 period does not look all that terribly great under this prism.

Now, to make things a bit more clear, here is the data from the chart above reproduced into one Alternative Real GDP measure.

As you can see, from this perspective of the two charts above, the ‘90s was an era of great economic prosperity with positive growth almost the entire decade. Once we drift into the ‘00s, however, we have continued negative economic growth from 2000 till 2006. At that point, dramatic falls in housing prices lowered the real cost of living, thereby creating real economic gains.

In fact, surprisingly, according to this conceptualization, we’ve had more real economic growth from 2006 to 2011 than we did from 2000 to 2006. This isn’t because the US economy was doing exceptionally well in the latter period so much as the drop in real estate prices allowed for sustainable economic growth to resume; albeit, with a huge overhang from a weakened banking system holding things back a bit and stifling employment.

Hence, from this perspective of Alternative CPI inflation, the first half of the ‘00s appears as if it would be more aptly called “the Great Stagflation.” It should not be perceived as a period of prosperity, but rather, an inflationary depression, caused by poor monetary policy, misguided housing incentives, and an unneeded stimulus from the Federal government that only made things worse.

The Great Stagflation

Looking back, this period should have never been considered a “boom period” at all. Rather, it may have been the classic case of demand-pull inflation. In demand-pull inflation, unemployment actually falls below the “full employment” level, so laborers demand significantly higher wages. Unfortunately the small increases in productivity at this level (i.e. aggregate supply) are outpaced by increases in aggregate demand. This drives up end prices, resulting in inflation.

As such, the Great Stagflation should be examined as a more than just a boom; but actually, a depressionary boom, where an oversupply of money in the economy created a situation where the overall economy was experiencing negative returns on investment.

This was ignored largely at the time because Americans fell for two myths:

In my next article, we’ll examine monetary policy and how it helped contributed to the Great Stagflation. source

Prior to 1983, the US Consumer Price Index included housing prices. A change was made at that time, however, to replace housing prices with a concept called “owners’ equivalent rent.” The rationale behind this change was that CPI should not include “investments” and home ownership was both consumption and investment. “Owners’ equivalent rent” was measured not by housing prices, but by rental prices given up by the homeowner in order to occupy the unit. In this way, it was hoped to strip out the “investment” related aspect of housing, while still holding onto the consumption aspect of it.

Unfortunately, this minor change in the way CPI was measured has had dramatic results on the end product. It’s created a situation where the Federal Reserve and other government actors are looking at one set of statistics to measure inflation, when the economic reality can be completely different. This is not to argue that there is a conspiracy to engineer the statistics, as some have suggested. Rather, a minor change in methodology has merely changed the way we perceive things in a detrimental fashion.

Alternative Economics

I’ve become enamored by how the disparity between official economic statistics and economic reality might have caused poor decision making by both the public sector and the private sector. As a result, I’ve launched a website, Alternative Economics, dedicated to exploring this issue in more detail. The centerpiece of my efforts is an Alternative CPI measure based on housing prices. From this, I’ve also re-examined GDP growth and monetary policy. The results have been paradigm-shifting, to say the least.

After viewing the economy under the lens of “Alternative CPI,” the US appears to have had negative real economic growth from 2000 to 2006. With high nominal GDP growth offset by even higher inflation, this period would be most properly termed “The Great Stagflation” or alternatively, “The Great Inflationary Depression.”

In this sense, 2000 – 2006 was the worst period in American economic history since the Great Depression and the ‘70s Stagflationary Era. While I’ve drawn several conclusions using my data, for now, I want to focus on my concept of Alternative CPI to show you why it’s more accurate and why it should change the way you think about the 2000s.

Alternative CPI Methodology

One major reason why housing price data is vital for any realistic inflation measure in the United States is because so much of American consumption is related to housing. Roughly 65% of Americans are homeowners and we have a society that views home ownership as an important goal in life. Mortgage payments often make up anywhere from 25% – 40% of monthly income for many Americans, making it a major cost.

Due to the effect of leverage in the housing market, it is one of the areas of consumer expenditure where prices are most likely to become inflated due to an excess supply of money. Given this, to ignore housing prices in inflationary measures is pure folly. Indeed, what’s the point of even examining CPI inflation if it ignores the most pertinent item in most American’s budgets?

For my conception of Alternative CPI, I’ve replaced the BLS’s concept of owners’ equivalent rent, with the S&P /Case-Shiller Home Price Index. This is slightly different than Floyd Norris’ conception in the NY Times, as he uses statistics compiled from Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB). I decided to use Case-Shiller over this for a few reasons, including greater ease of access. Moreover, I would view it as an acceptable proxy for housing prices across the country.

In spite of the fact that urban housing prices would tend to rise more in a boom than rural prices, the majority of the American populace lives in a major metropolitan area. Urban housing prices would also be a better indicator of dangers in the real economy.

With Case-Shiller, there is both a 10-city index and a 20-city index. The 10-city index has a longer history, going back to 1987, while the 20-city index only reaches back to 2000. The obvious advantage with the 20-city index is that it looks at a broader swath of housing data. However, in practice, the two indexes do not dramatically differ from one another, as the chart below suggests - (click charts to enlarge):

While the Case-Shiller 10-city index does show slightly higher year-over-year increases during the housing boom years, the differences are not that dramatic. In fact, if we take the above chart and add the BLS’s concept of “Owners’ Equivalent Rent” (OER), you will quickly see that the differences between the two Case-Shiller indices are minor compared with the difference between Case-Shiller housing price data and “Owners’ Equivalent Rent.”

Given this, I decided to use Case-Shiller’s 10-city housing price index in order to calculate Alternative CPI. The longer history associated with that index creates a better data set and it’s not a stretch to suggest that the Case-10 can serve as a proxy for a broader metropolitan housing market index.

Before jumping to the results of our Alternative CPI, let’s take a look at one final chart examining the Case-Shiller Index versus owners’ equivalent rent. The chart below shows the index values, as opposed to year-over-year increases as in the chart above. The giant hill in the chart represents the housing bubble and you can see that we are just now reaching a point where the Case-Shiller 10-city index and OER are finally closing in on one another again:

Alternative CPI

Due to the failure of OER to capture true price inflation, it’s easy to see why Alternative CPI ends up being such an important concept. OER allowed official inflation figures to be dramatically understated for years and might have hidden major economic problems in the United States during the early 2000s. Moreover, it led to extremely poor policymaking from the Federal Reserve and the US government.

Let’s examine how Alternative CPI differs from official CPI. For my measure, I did not change any inputs in official CPI inflation except OER, which I replaced with the Case-Shiller 10-city housing price index. With this one minor change, CPI looks dramatically different as the chart below shows:

Official CPI and Alternative CPI stay within about a 200 basis point spread of one another from 1988 to 1998. After that, the two figures start to drift apart considerably. By 2004, there is nearly a 700 basis point spread between official CPI and our Alternative CPI measure.

In July ’04, for instance, official CPI records a mild 3.0% year-over-year increase in inflation. While this is lower than the Federal Reserve’s general target, it’s not all that alarming, all the same. 3% is well within US historical averages during healthy economic times.

Alternative CPI, on the other hand, reports a troubling 9.4% year-over-year increase in inflation. If official CPI had reported such a high result, alarm bells would’ve been set off all over the place. 3% is manageable inflation; 9.4% suggests an economy with major problems. In fact, we had already drifted over 6% inflation in 1999 using my Alternative CPI gauge. Alternative CPI cooled off a bit during the tech crash, before eclipsing 6% inflation once again by mid-2002.

Alternative Real GDP

Where this becomes even more profound is when we start looking at the Alternative CPI inflation compared with economic growth and monetary policy. I’m saving the monetary policy discussion for my next article, so for now, we’ll focus on economic growth. This is where our Alternative CPI starts to become “paradigm-shifting.” The chart below examines Alternative CPI versus Nominal GDP:

The best way to read the chart above is to examine both lines to see which one is on top. When the blue line is above the red line, that means that the US was experiencing positive real economic growth. When the blue line is below the red line, that means that price increases were outpacing nominal GDP growth, so that real economic growth was negative. Notice that the 2000 to 2006 period does not look all that terribly great under this prism.

Now, to make things a bit more clear, here is the data from the chart above reproduced into one Alternative Real GDP measure.

As you can see, from this perspective of the two charts above, the ‘90s was an era of great economic prosperity with positive growth almost the entire decade. Once we drift into the ‘00s, however, we have continued negative economic growth from 2000 till 2006. At that point, dramatic falls in housing prices lowered the real cost of living, thereby creating real economic gains.

In fact, surprisingly, according to this conceptualization, we’ve had more real economic growth from 2006 to 2011 than we did from 2000 to 2006. This isn’t because the US economy was doing exceptionally well in the latter period so much as the drop in real estate prices allowed for sustainable economic growth to resume; albeit, with a huge overhang from a weakened banking system holding things back a bit and stifling employment.

Hence, from this perspective of Alternative CPI inflation, the first half of the ‘00s appears as if it would be more aptly called “the Great Stagflation.” It should not be perceived as a period of prosperity, but rather, an inflationary depression, caused by poor monetary policy, misguided housing incentives, and an unneeded stimulus from the Federal government that only made things worse.

The Great Stagflation

Looking back, this period should have never been considered a “boom period” at all. Rather, it may have been the classic case of demand-pull inflation. In demand-pull inflation, unemployment actually falls below the “full employment” level, so laborers demand significantly higher wages. Unfortunately the small increases in productivity at this level (i.e. aggregate supply) are outpaced by increases in aggregate demand. This drives up end prices, resulting in inflation.

As such, the Great Stagflation should be examined as a more than just a boom; but actually, a depressionary boom, where an oversupply of money in the economy created a situation where the overall economy was experiencing negative returns on investment.

This was ignored largely at the time because Americans fell for two myths:

- Low unemployment signals a healthy economy

- Official CPI showed very low inflation, relative to economic growth

In my next article, we’ll examine monetary policy and how it helped contributed to the Great Stagflation. source

Wednesday, June 22, 2011

‘Shadow’ Inventory of Homes Dips

The National Association of Realtors reported yesterday that there are 3.72 million homes now listed for sale, which works out to a stiff nine-months backlog of unsold homes given the current anemic sales pace. That backlog is 50 percent more than the six-month level that is considered normal for a healthy market. Not too much to cheer there.

But a report released today that tracks the nation’s “shadow” inventory of foreclosed homes that have yet to hit the market, as well as homes in the foreclosure pipeline and those whose owners are seriously delinquent, offers a glimmer of hope. CoreLogic reports today that as of the end of April, there were 1.7 million homes in its shadow inventory database, down from 1.9 million a year ago. Moreover, the current shadow inventory is now 18 percent below it’s all-time high in January 2010.

The Less-Bad Housing Market

To be clear, these are still god-awful ugly statistics. There’s no way you can state with a straight face that there is anything good about shadow inventory of 1.7 million. On its own, the shadow inventory represents a five-month supply, or just one month short of what would be healthy inventory for the entire market. But the fact that the shadow inventory trend seems to be less-bad is an encouraging sign that the worst may be over. CoreLogic also reports that the combined total of regular “visible” inventory plus shadow inventory is 5.7 million homes. That’s well more than a year’s worth of supply, but even that ugly data point is 6.2 percent lower than where it stood a year ago.

Mark Fleming, chief economist for CoreLogic noted that a decline in the flow of delinquent loans is a big part of the story here. LPS Applied Analytics, which tracks nearly 40 million mortgages, issued a preliminary report yesterday showing that the mortgage delinquency rate (mortgages at least 30 days late) in May was 18 percent lower than a year earlier. And a joint report from S&P/Experian out yesterday shows the default rate on first mortgages in April is nearly 40 percent below the year-earlier level.

Still, no one is breaking out any champagne. As CoreLogic’s Fleming pointed out, “it will probably take several years for the shadow inventory to be absorbed given the long timelines in processing and completing foreclosures.”

That may well be true. But as noted in 7 Reasons Why Now is a Good Time to Buy a Home, not every state is buried in foreclosures. For example, while 53 percent of recent sales in Nevada were foreclosures, they represent just 7 percent of the New York state sales.

The Big Wild Card

There is one other market driver that could spell the most surprise for the housing market, and not in a good way. CoreLogic reports that there are nearly 11 million homeowners with negative equity, meaning their mortgage is higher than their home’s value. And 2 million of those underwater homeowners are more than 50 percent underwater. Those are the big wild cards in whether the recent less-bad news about the housing market continues, or we get smacked with another leg down. And a lot of that is going to be determined not so much by the housing market itself, but whether the economic soft patch doesn’t ossify and we’re able get some meaningful job growth.

But again, just as with the foreclosure data, the negative equity story is also skewed by what’s going on a few of the hardest hit states. CoreLogic says that 22.7 percent of all homeowners are underwater. But looking at just the most troubled states — Arizona, Florida, Michigan, and California — the share of homeowners that are under water jumps to 39 percent. Outside of those five states, the negative equity share is a still bad (but not nearly as bad) 16 percent. - By Carla Fried

But a report released today that tracks the nation’s “shadow” inventory of foreclosed homes that have yet to hit the market, as well as homes in the foreclosure pipeline and those whose owners are seriously delinquent, offers a glimmer of hope. CoreLogic reports today that as of the end of April, there were 1.7 million homes in its shadow inventory database, down from 1.9 million a year ago. Moreover, the current shadow inventory is now 18 percent below it’s all-time high in January 2010.

The Less-Bad Housing Market

To be clear, these are still god-awful ugly statistics. There’s no way you can state with a straight face that there is anything good about shadow inventory of 1.7 million. On its own, the shadow inventory represents a five-month supply, or just one month short of what would be healthy inventory for the entire market. But the fact that the shadow inventory trend seems to be less-bad is an encouraging sign that the worst may be over. CoreLogic also reports that the combined total of regular “visible” inventory plus shadow inventory is 5.7 million homes. That’s well more than a year’s worth of supply, but even that ugly data point is 6.2 percent lower than where it stood a year ago.

Mark Fleming, chief economist for CoreLogic noted that a decline in the flow of delinquent loans is a big part of the story here. LPS Applied Analytics, which tracks nearly 40 million mortgages, issued a preliminary report yesterday showing that the mortgage delinquency rate (mortgages at least 30 days late) in May was 18 percent lower than a year earlier. And a joint report from S&P/Experian out yesterday shows the default rate on first mortgages in April is nearly 40 percent below the year-earlier level.

Still, no one is breaking out any champagne. As CoreLogic’s Fleming pointed out, “it will probably take several years for the shadow inventory to be absorbed given the long timelines in processing and completing foreclosures.”

That may well be true. But as noted in 7 Reasons Why Now is a Good Time to Buy a Home, not every state is buried in foreclosures. For example, while 53 percent of recent sales in Nevada were foreclosures, they represent just 7 percent of the New York state sales.

The Big Wild Card

There is one other market driver that could spell the most surprise for the housing market, and not in a good way. CoreLogic reports that there are nearly 11 million homeowners with negative equity, meaning their mortgage is higher than their home’s value. And 2 million of those underwater homeowners are more than 50 percent underwater. Those are the big wild cards in whether the recent less-bad news about the housing market continues, or we get smacked with another leg down. And a lot of that is going to be determined not so much by the housing market itself, but whether the economic soft patch doesn’t ossify and we’re able get some meaningful job growth.

But again, just as with the foreclosure data, the negative equity story is also skewed by what’s going on a few of the hardest hit states. CoreLogic says that 22.7 percent of all homeowners are underwater. But looking at just the most troubled states — Arizona, Florida, Michigan, and California — the share of homeowners that are under water jumps to 39 percent. Outside of those five states, the negative equity share is a still bad (but not nearly as bad) 16 percent. - By Carla Fried

California May Home Sales an estimated 35,536 were Sold

An estimated 35,536 new and resale houses and condos were sold statewide last month. That was up 0.9 percent from 35,202 sales in April, and down 13.3 percent from 40,965 sales in May 2010. California sales for the month of May have varied from a low of 32,223 in 1995 to a high of 67,958 in 2004, while the average is 46,840. DataQuick's statistics go back to 1988.

The median price paid for a home in California last month was $249,000, unchanged from April, and down 10.4 percent from $278,000 in May 2010. The year-over-year decrease was the eighth in a row after 11 months of increases. The last time the median fell more on a year-over-year basis was in September 2009, when it fell 11.3 percent. The statewide median’s low point in the current cycle was $221,000 in April 2009, while the peak was $484,000 in early 2007.

Distressed property sales made up about 53 percent of California’s resale market last month.

Of the existing homes sold in May, 35.5 percent were properties that had been foreclosed on during the prior 12 months. That was down from 36.4 percent in April and about the same as 35.4 percent in May 2010. The all-time high was 58.5 percent in February 2009.

Short sales – transactions where the sale price fell short of what was owed on the property – made up an estimated 17.9 percent of resales last month. That was up from and estimated 16.9 percent in April but down from 18.9 percent a year earlier. Two years ago short sales made up 12.2 percent of the resale market.

The typical mortgage payment that home buyers committed themselves to paying last month was $1,025. That was down from $1,050 in April and and down from $1,178 in May 2010. Adjusted for inflation, last month's mortgage payment was 53.8 percent below the spring 1989 peak of the prior real estate cycle. It was 61.5 percent below the current cycle's peak in June 2006.

San Diego-based DataQuick monitors real estate activity nationwide and provides information to consumers, educational institutions, public agencies, lending institutions, title companies and industry analysts.

Indicators of market distress continue to move in different directions. Foreclosure activity has declined somewhat but remains high by historical standards. Financing with multiple mortgages is low, down payment sizes are stable, cash and non-owner occupied buying has eased a bit this spring but remains relatively high, DataQuick reported. - DQNews

The median price paid for a home in California last month was $249,000, unchanged from April, and down 10.4 percent from $278,000 in May 2010. The year-over-year decrease was the eighth in a row after 11 months of increases. The last time the median fell more on a year-over-year basis was in September 2009, when it fell 11.3 percent. The statewide median’s low point in the current cycle was $221,000 in April 2009, while the peak was $484,000 in early 2007.

Distressed property sales made up about 53 percent of California’s resale market last month.

Of the existing homes sold in May, 35.5 percent were properties that had been foreclosed on during the prior 12 months. That was down from 36.4 percent in April and about the same as 35.4 percent in May 2010. The all-time high was 58.5 percent in February 2009.

Short sales – transactions where the sale price fell short of what was owed on the property – made up an estimated 17.9 percent of resales last month. That was up from and estimated 16.9 percent in April but down from 18.9 percent a year earlier. Two years ago short sales made up 12.2 percent of the resale market.

The typical mortgage payment that home buyers committed themselves to paying last month was $1,025. That was down from $1,050 in April and and down from $1,178 in May 2010. Adjusted for inflation, last month's mortgage payment was 53.8 percent below the spring 1989 peak of the prior real estate cycle. It was 61.5 percent below the current cycle's peak in June 2006.

San Diego-based DataQuick monitors real estate activity nationwide and provides information to consumers, educational institutions, public agencies, lending institutions, title companies and industry analysts.

Indicators of market distress continue to move in different directions. Foreclosure activity has declined somewhat but remains high by historical standards. Financing with multiple mortgages is low, down payment sizes are stable, cash and non-owner occupied buying has eased a bit this spring but remains relatively high, DataQuick reported. - DQNews

Saturday, June 4, 2011

Slow-moving economy runs into 'brick wall'

By John W. Schoen - Policymakers, investors and economic forecasters are hoping that a sharp slowdown in economic growth last month was only a speed bump on an already bumpy road to recovery.

Because otherwise the ride could get a whole lot rougher.Friday's jobs numbers showed that the economy produced a meager 54,000 new jobs in May with weakness across all sectors. The data capped a week of reports pointing to a sudden, unexpected slowdown in the recovery.

"It is now pretty clear that the economy ran into a brick wall last month," said Paul Ashworth, chief U.S. economist at Capital Economics.

Prior to this week most data had been pointing to a slow but steady increase in the economy's momentum. What took the wind out of the recovery's sails so suddenly, and will the doldrums last?

On top of the list is a surge in gasoline prices that has forced consumers to tighten spending on the rest of their household budget. Job growth in the retail, leisure and hospitality industries, which had been showing healthy advances, ground to a halt last month.

Floods and deadly tornadoes shut down some businesses in the southern half of the nation last month and may have depressed the jobs count. Some analysts also pointed to a slowdown in U.S. manufacturing because of a shortage of parts as Japanese suppliers continue to rebuild after a devastating earthquake in March.

The impact of those factors should dissipate in the summer and fall. Japanese suppliers are rebuilding faster than initial estimates suggested. In the past month, oil prices have fallen from a peak of $114 a barrel to under $100. Gasoline prices are beginning to ease off too; the average pump price is down 4 percent from a peak of $3.97 a gallon just two weeks ago.

Once those forces are no longer holding back growth, many analysts believe, the economy's underlying strength will restore momentum and get the recovery and job growth back on track.

There are troubling signs, though, that the recovery faces more fundamental, long-term threats. That list begins with the failure of Congress to give the Treasury legal authority to borrow enough money to pay all the government's expenses.

On Thursday, a second major credit rating agency warned Congress and the White House that if they don't agree on a way to raise the nation's borrowing limit, the U.S. government could lose its top debt rating. Such a downgrade would likely force up interest rates and raise borrowing costs, creating a headwind strong enough to increase the risk of another recession.

"We don't have a very positive outlook for job creation in the next few months," said William Dunkelberg, chief economist at the the National Federation of Independent Businesses, whose members this week reported in a monthly survey that they're cutting back on hiring plans. "The big issue for us is confidence. We don't have any confidence in the leadership that they're going to solve this problem."

The solution itself could spell trouble. At roughly $1.5 trillion, the federal budget deficit represents about 10 percent of gross domestic product. Closing that deficit too quickly, with either deep spending cuts, tax increases or both, could send the economy back into recession. Spending cuts by cash-strapped state and local governments have already eliminated nearly 450,000 jobs since September 2008.

In May, state and local governments cut 28,000 jobs, the most since November, while private businesses hired only 83,000 new workers.

Perhaps the biggest force holding back the recovery is the housing market, still mired in its deepest downturn since the Great Depression. There was no improvement in May, as home builders sat on the sidelines for the fifth spring since the housing market collapsed in late 2006.

"In every cycle we have come out of, construction has always been a major factor in the recovery, going back to the end of World War II and even back to the '30s," former Federal Reserve Chairman Alan Greenspan told CNBC Friday. "This is the first time when construction has not come out of this."

The collapse of the housing market has stunted job growth for several reasons. Apart from begetting jobs directly in building trades, new home construction creates related jobs in fields such as real estate sales and mortgage lending. Growth in demand for home furnishings and appliances has also been hurt.

More broadly, falling home prices are robbing American consumers of their savings and weighing on consumer confidence. Home values are in free-fall in many parts of the country as lenders struggle to unload millions of foreclosed properties by sharply cutting prices. Housing industry analysts say that the foreclosure pipeline will take several more years to clear.

Even if the latest "pause" in job growth is temporary, the pace of hiring is expected to remain painfully slow. Economists are still debating why the current recovery has been so sluggish. But nearly two years after the recession ended, the rebound is far slower than past recoveries.

"This remains a horribly weak economic recovery. We're still looking at payrolls today that show 7 million fewer jobs compared to the peak of January 2008," said John Lonski, an economist at Moody's Capital Markets Group. "Until we make more progress on the jobs front, until we start to generate jobs at a rate of at least 300,000 to 350,000 per month, we're going to be disappointed with the pace of activity."

Friday, June 3, 2011

Home sales fall in Orange County

by Jon Lansner - For the 22 business days ending May 20 – DataQuick’s freshest stats — the Orange County real estate market had homebuying patterns showing:

| Slice | Price | Ch. | Sold | Ch. |

|---|---|---|---|---|

| House | $500,000 | -5% | 1,752 | -16% |

| Condo | $270,000 | -10% | 794 | -20% |

| New | $540,500 | -16% | 198 | -10% |

| All OC | $425,000 | -4% | 2,744 | -17% |

- 26 of O.C.’s 83 ZIP codes with gains in their respective median selling price. Overall, buyers’ prices were -4.5% vs. a year ago.

- Taking sales volume in consideration, home-sale pricing is up in ZIPs representing 26% of the Orange County market.

- 6 of 83 O.C. ZIPs with median sales prices above $1 million in the period vs. 11 million-dollar ZIPs when the county median price peaked in June 2007. Since that pricing pinnacle, there’s been a 34% drop in the countywide median price!

- Current million-dollar ZIPs were 4% of all sales in the most recent period tracked.

- There were 4 ZIPs with medians under $250,000 vs. 4 a year ago. ZIPs with medians under a quarter million had 4% of all sales in the most recent period.

- 60 of 83 O.C. ZIPs had year-over-year sales declines in the period — or 72% of the market.

- Overall, countywide sales were down 16.6% vs. a year ago.

- 1 of 83 O.C. ZIPs has sales gains of 100% or more in the period at the same time as 4 had sales drops greater than 50%!

- NOTE! 7 local ZIPs had both sales gains and price gains in the period. (Highlighted in green below!) These double-gainers had combined sales volume equal to 7% of the Orange County market.

Also, want to see what kind of housing the median price buys in a specific neighborhood? Click on the ZIP code, and you’ll see current for-sale listings in the median’s “ballpark” — a range from 10% below to 10% above — in that ZIP …

| Town | ZIP | Price | Yr. chg. | Sales | Yr. chg. |

|---|---|---|---|---|---|

| Aliso Viejo | 92656 | $345,000 | -17.7% | 77 | -31.3% |

| Anaheim | 92801 | $300,000 | -6.3% | 29 | -27.5% |

| Anaheim | 92802 | $320,000 | -1.8% | 17 | -26.1% |

| Anaheim | 92804 | $300,000 | -12.8% | 38 | -25.5% |

| Anaheim | 92805 | $307,000 | +2.3% | 32 | -22.0% |

| Anaheim | 92806 | $360,000 | -7.7% | 25 | +47.1% |

| Anaheim | 92807 | $418,500 | -11.0% | 38 | +35.7% |

| Anaheim | 92808 | $391,000 | -15.9% | 20 | -42.9% |

| Brea | 92821 | $450,000 | -4.3% | 19 | -26.9% |

| Brea | 92823 | $789,500 | +8.9% | 8 | +100.0% |

| Buena Park | 90620 | $342,500 | -17.0% | 28 | -36.4% |

| Buena Park | 90621 | $350,000 | -3.3% | 20 | +17.6% |

| Corona del Mar | 92625 | $1,650,000 | -5.4% | 27 | -6.9% |

| Costa Mesa | 92626 | $525,000 | +3.5% | 29 | +3.6% |

| Costa Mesa | 92627 | $405,000 | -4.7% | 38 | -25.5% |

| Cypress | 90630 | $450,000 | -0.6% | 30 | -31.8% |

| Dana Point | 92624 | $455,000 | -17.3% | 7 | -36.4% |

| Dana Point | 92629 | $595,000 | +0.8% | 41 | -6.8% |

| Foothill Ranch | 92610 | $323,500 | +1.1% | 18 | -25.0% |

| Fountain Valley | 92708 | $549,500 | -4.4% | 32 | -45.8% |

| Fullerton | 92831 | $356,000 | -2.2% | 19 | -9.5% |

| Fullerton | 92832 | $322,500 | -5.7% | 18 | -14.3% |

| Fullerton | 92833 | $370,000 | -2.6% | 35 | -39.7% |

| Fullerton | 92835 | $490,000 | -0.5% | 19 | -5.0% |

| Garden Grove | 92840 | $311,000 | -10.5% | 28 | -41.7% |

| Garden Grove | 92841 | $355,000 | -2.1% | 20 | -23.1% |

| Garden Grove | 92843 | $269,500 | -20.3% | 30 | -21.1% |

| Garden Grove | 92844 | $317,500 | -2.3% | 12 | -61.3% |

| Garden Grove | 92845 | $420,000 | -14.1% | 11 | -35.3% |

| Huntington Beach | 92646 | $415,000 | -21.0% | 64 | -24.7% |

| Huntington Beach | 92647 | $475,000 | -6.9% | 36 | -7.7% |

| Huntington Beach | 92648 | $690,000 | -11.0% | 44 | -4.3% |

| Huntington Beach | 92649 | $480,000 | -15.0% | 34 | -5.6% |

| Irvine | 92602 | $660,000 | +2.6% | 15 | -50.0% |

| Irvine | 92603 | $1,075,000 | +21.8% | 30 | +11.1% |

| Irvine | 92604 | $501,000 | -4.6% | 30 | +3.4% |

| Irvine | 92606 | $520,000 | +17.1% | 18 | -10.0% |

| Irvine | 92612 | $421,000 | -11.2% | 43 | -10.4% |

| Irvine | 92614 | $331,000 | -38.7% | 23 | -20.7% |

| Irvine | 92618 | $563,318 | -4.0% | 62 | +26.5% |

| Irvine | 92620 | $582,750 | -16.8% | 52 | -17.5% |

| Ladera Ranch | 92694 | $533,000 | -1.3% | 50 | -29.6% |

| La Habra | 90631 | $305,000 | -6.7% | 53 | -5.4% |

| La Palma | 90623 | $495,000 | -11.6% | 9 | -35.7% |

| Laguna Beach | 92651 | $1,052,500 | +4.7% | 27 | -38.6% |

| Laguna Hills | 92653 | $440,000 | -11.1% | 31 | +0.0% |

| Laguna Niguel | 92677 | $497,750 | +0.3% | 103 | -8.8% |

| Laguna Woods | 92637 | $220,000 | +37.5% | 36 | +24.1% |

| Lake Forest | 92630 | $406,250 | +12.8% | 51 | -20.3% |

| Los Alamitos | 90720 | $725,000 | +9.8% | 9 | -40.0% |

| Midway City | 92655 | $340,000 | +51.1% | 2 | -77.8% |

| Mission Viejo | 92691 | $424,000 | -3.9% | 63 | +23.5% |

| Mission Viejo | 92692 | $450,000 | -9.1% | 59 | -25.3% |

| Newport Beach | 92660 | $980,000 | +4.3% | 43 | -6.5% |

| Newport Beach | 92661 | $2,825,000 | +61.4% | 3 | -57.1% |

| Newport Beach | 92662 | $3,525,000 | +101.4% | 2 | -60.0% |

| Newport Beach | 92663 | $850,000 | +18.9% | 26 | +13.0% |

| Newport Coast | 92657 | $1,422,500 | -25.1% | 23 | -25.8% |

| Orange | 92865 | $400,000 | -12.3% | 22 | -31.3% |

| Orange | 92866 | $432,000 | -1.8% | 13 | +30.0% |

| Orange | 92867 | $433,000 | -15.8% | 39 | +5.4% |

| Orange | 92868 | $245,000 | -10.9% | 14 | +55.6% |

| Orange | 92869 | $451,000 | +9.7% | 30 | -18.9% |

| Placentia | 92870 | $445,000 | -2.2% | 41 | +5.1% |

| Rancho Santa Margarita | 92688 | $382,500 | +10.9% | 64 | -32.6% |

| San Clemente | 92672 | $461,000 | -18.8% | 29 | -34.1% |

| San Clemente | 92673 | $668,750 | -1.7% | 52 | +15.6% |

| San Juan Capistrano | 92675 | $312,000 | -13.1% | 35 | -23.9% |

| Santa Ana | 92701 | $220,000 | +63.0% | 21 | -36.4% |

| Santa Ana | 92703 | $259,000 | -11.5% | 39 | +21.9% |

| Santa Ana | 92704 | $298,750 | +1.3% | 46 | -38.7% |

| Santa Ana | 92705 | $398,500 | -36.2% | 53 | +35.9% |

| Santa Ana | 92706 | $353,000 | -1.7% | 15 | -46.4% |

| Santa Ana | 92707 | $242,000 | -2.2% | 43 | -25.9% |

| Seal Beach | 90740 | $660,000 | +36.1% | 13 | +18.2% |

| Stanton | 90680 | $251,250 | -7.8% | 23 | +0.0% |

| Trabuco/Coto | 92679 | $662,000 | +12.2% | 52 | +2.0% |

| Tustin | 92780 | $418,000 | +11.5% | 35 | -23.9% |

| Tustin | 92782 | $588,500 | +0.2% | 38 | -15.6% |

| Villa Park | 92861 | $740,000 | -23.1% | 7 | +16.7% |

| Westminster | 92683 | $421,500 | -0.2% | 52 | -27.8% |

| Yorba Linda | 92886 | $610,000 | -4.7% | 53 | -28.4% |

| Yorba Linda | 92887 | $600,000 | -5.5% | 32 | -3.0% |

| Total O.C. | $425,000 | -4.5% | 2,744 | -16.6% |

Is Now A Good Time To Invest In Real Estate?

- Although mortgage rates have recently risen slightly from their all-time lows, the recovery of the housing market is not a reality in many areas of the United States. This means that houses in several different states cost less than they have in years and rates are still low enough to make investing in real estate a popular consideration for many investors. But is this really a good time to be investing in property that you won't be living in? After all, there are many things to consider beyond the opportunistic aspects of the decision.

Carrying CostsCarrying costs for an empty property meant for resale don't just include the monthly mortgage payment. They also include insurance costs, property taxes, upkeep and repair expenses. Even if you plan on renting the property before it is sold, you still need to have adequate cash reserves to pay all of these expenses because the rent you are able to charge in your area might not be enough to provide adequate resources. Finally, consider how long you may need to cover these costs. When the housing market was booming and houses were easily flipped, carrying costs might not have been a concern; but now, when houses can sit on the market for months or years, they are.

Risk and ReturnThe discussion above about carrying costs gives an indication of the amount of risk you might be taking on when you invest in real estate. Conventional investing wisdom says that real estate is an investment that will grow over time, but recent years have shown that this growth may not be as straight forward as an investor might want. Additionally, after paying the mortgage interest, insurance, property taxes and maintenance expenses for a number of years, the return made when you sell the property for more than you purchased it for could be much less than you anticipated because your cost basis is comprised of more expenses than just purchase price and interest.

LiquidityReal estate is not generally considered a liquid investment because it is not easily sold for cash, and in a restrictive financial environment, real estate is even more illiquid. Even if you just need to pull some equity out for an emergency, assuming you have any equity,the restrictive lending environment could mean that you have difficulty accessing any cash.

Investing GoalsYour personal investing goals and timeline will have a lot of bearing on whether or not real estate is a good investment for you right now. If you are within a few years of retirement, investing in real estate could actually push your retirement back until a later date, especially if you tap into your retirement savings for the down payment. In addition, if you have to carry the property for a great deal of time, it could reduce the amount of money you can save and your subsequent earnings on those savings. If you have a longer-term saving plan, then you might have more flexibility to add something as unpredictable as real estate to your financial plan.

The Bottom LineOften, a "good time to buy" for one investor may not be for another. Sure, opportunities for return abound, but if it isn't actually a good time for you to invest then the opportunities that you see will not be something that you can trust to provide an opportunity to you. Instead, they may turn into financial mistakes and burdens that you have trouble keeping up with. When evaluating the potential of investing in real estate, don't just think about home prices and interest rates; take the time to consider your personal financial situation and whether or not you can afford the long-term commitment a real estate investment might entail.

- San Francisco Chronicle

Carrying CostsCarrying costs for an empty property meant for resale don't just include the monthly mortgage payment. They also include insurance costs, property taxes, upkeep and repair expenses. Even if you plan on renting the property before it is sold, you still need to have adequate cash reserves to pay all of these expenses because the rent you are able to charge in your area might not be enough to provide adequate resources. Finally, consider how long you may need to cover these costs. When the housing market was booming and houses were easily flipped, carrying costs might not have been a concern; but now, when houses can sit on the market for months or years, they are.

Risk and ReturnThe discussion above about carrying costs gives an indication of the amount of risk you might be taking on when you invest in real estate. Conventional investing wisdom says that real estate is an investment that will grow over time, but recent years have shown that this growth may not be as straight forward as an investor might want. Additionally, after paying the mortgage interest, insurance, property taxes and maintenance expenses for a number of years, the return made when you sell the property for more than you purchased it for could be much less than you anticipated because your cost basis is comprised of more expenses than just purchase price and interest.

LiquidityReal estate is not generally considered a liquid investment because it is not easily sold for cash, and in a restrictive financial environment, real estate is even more illiquid. Even if you just need to pull some equity out for an emergency, assuming you have any equity,the restrictive lending environment could mean that you have difficulty accessing any cash.

Investing GoalsYour personal investing goals and timeline will have a lot of bearing on whether or not real estate is a good investment for you right now. If you are within a few years of retirement, investing in real estate could actually push your retirement back until a later date, especially if you tap into your retirement savings for the down payment. In addition, if you have to carry the property for a great deal of time, it could reduce the amount of money you can save and your subsequent earnings on those savings. If you have a longer-term saving plan, then you might have more flexibility to add something as unpredictable as real estate to your financial plan.

The Bottom LineOften, a "good time to buy" for one investor may not be for another. Sure, opportunities for return abound, but if it isn't actually a good time for you to invest then the opportunities that you see will not be something that you can trust to provide an opportunity to you. Instead, they may turn into financial mistakes and burdens that you have trouble keeping up with. When evaluating the potential of investing in real estate, don't just think about home prices and interest rates; take the time to consider your personal financial situation and whether or not you can afford the long-term commitment a real estate investment might entail.

- San Francisco Chronicle

Subscribe to:

Comments (Atom)